Jay Powell has spent the last 3 hours in the Senate answering questions how long until the US slides into recession (really, it’s mostly been a filibuster by Dems on the Senate Banking Committee explaining to Powell how Biden is not responsible for soaring inflation), but a much better question is “whether the US is already in a recession”, especially since the .Bloomberg Econ model now sees 98% odds of a recession in 24 months (up from 75% just a few days ago).

Jay Powell has spent the last 3 hours in the Senate answering questions how long until the US slides into recession (really, it’s mostly been a filibuster by Dems on the Senate Banking Committee explaining to Powell how Biden is not responsible for soaring inflation), but a much better question is “whether the US is already in a recession”, especially since the .Bloomberg Econ model now sees 98% odds of a recession in 24 months (up from 75% just a few days ago).

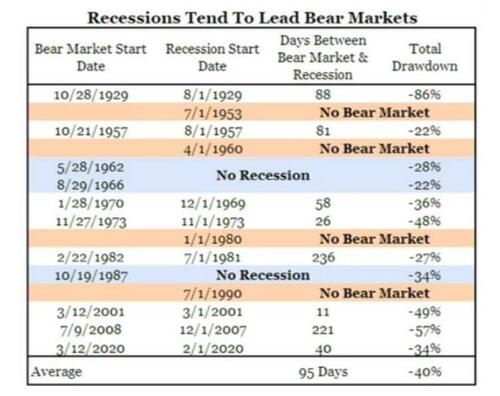

The first to answer this question is Piper Sandler, which answers “perhaps” and shows that the typical bear market follows the start of a recession with a delay of 95 days, and eventually exhaust itself with an average total drawdown of 40%..

…which means that current recession probably already started some time in March and has another 20% or so to go (to hit the 3,000 bogey that so many have mentioned in recent days).

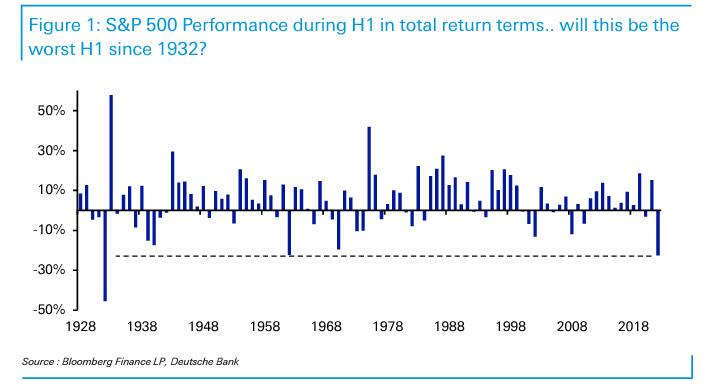

Of course, following the worst start for stocks to a year since the Great Depression…

…and also the worst start since 1932 in total return terms across all asset classes…

…one would be excused to ask if instead of a garden variety recession, the US isn’t rushing straight into a depression.

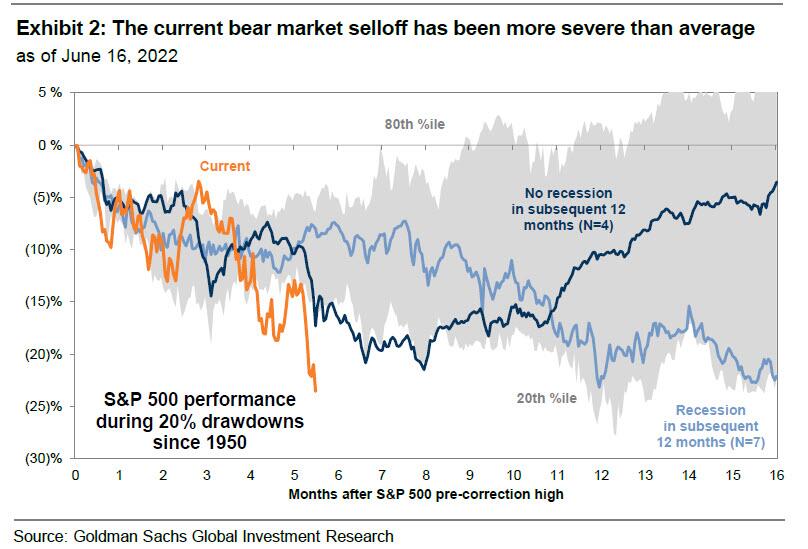

A slightly different perspective comes from Morgan Stanley, whose chief equity strategist Michael Wilson writes that the bank’s clients continue to debate whether we will see a recession in the next 12 months (one which may have already started), and whether it be a formal economic recession or an earnings recession. Understandably, the second most popular question asked by clients is what is the floor value – or worst case scenario – in terms of price. How low can equities trade in the event of a recession and what is already priced?

Morgan Stanley responds to these question in terms of industry group drawdowns during the past four recessions. The first thing to note is that price action suggests that equities have already drawn down ~60% of the recessionary average…

…with today’s price action relatively similar to recent recessions in terms of leadership, albeit less severe up to this point.

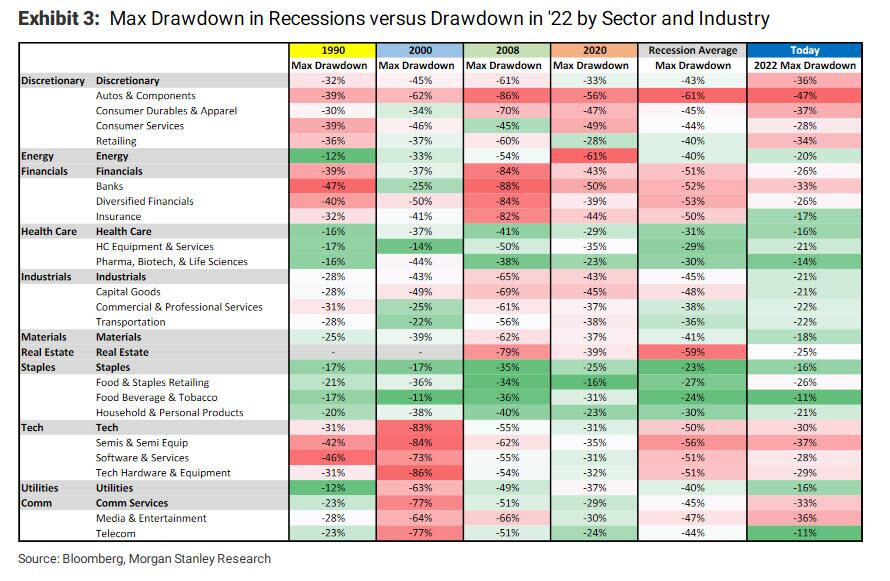

Consumer Discretionary and Food & Staples Retailing are the closest to a typical recessionary drawdown at 86% and 95% of average. On the flip side, the industry groups that are holding up the best in 2022 relative to the average recession are Telecom at 26% (which underperformed by 37% in 2021), Insurance at 34%, and Utilities at 41%.

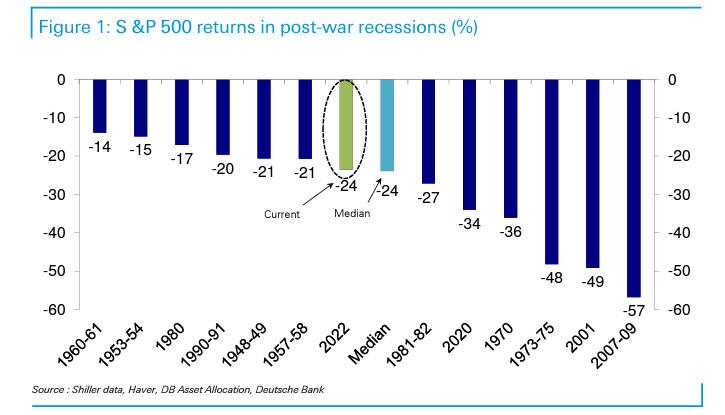

Finally, we turn to Deutsche Bank whose head of thematic research Jim Reid writes that following the latest selloff which dragged the market down 24% from its all time high, the S&P 500’s correction moved in line with the median correction seen in post-WWII recessions, and is now in fact the fourth worst non-recession correction over the same period. This is shown in a chart first used by DB’s equity strategist Binky Chadha a few weeks ago at the same time of his call that the S&P was likely to hit the median recession correction levels equivalent to 3650 in the coming weeks. Well, last week we did just that.

That said, as with Morgan Stanley, so Deutsche Bank notes that the timing of the recession is a hot topic at the moment, and when it hits, both Reid and Chadha expect the S&P 500 to be down -35 to -40% from the highs. The rationale being that the initial overvaluation was more extreme than normal cycles, with the additional comment that this recession marks a regime shift from decades of declining inflation to higher structural levels: “This deserves a bigger de-rating than average.”

However, the timing of that recession is important. According to Reid, if it occurs this year then markets will have a very tough H2 (spoiler alert: it will). However if miraculously the recession doesn’t happen until deeper into 2023, then markets can have notable relief rallies on the way (Reid still leans toward next year).

And if there is still anyone out there who thinks we can avoid a recession completely, then the three biggest post-WWII non-recession corrections are the -26.6% (May 1946-), -28% (Dec 1961-) and -33.5% (Aug 1987-). The last of these included the 1987 stock market crash. So if we don’t get a recession, we are getting close to extreme territory.

Unfortunately, we will…

**By Tyler Durden

**Source

The “recession” started in 1964 when the Silver Certificates we’re stopped. Gas was 25.9. Five and Dime Stores were everywhere. A soda pop was a dime. But in 1972 when “we” went off the Gold Standard gas went over a dollar. Then… Well you know the rest.